Industry Report: How Chinese OEMs Build Western Tech Organisations to Compete in the West.

How Chinese EV makers are establishing Western tech hubs to compete with Western OEMs & how Western OEMs can respond

Automotive

06 May 2024

Calle Unnérus

How Chinese EV makers are establishing Western tech hubs to compete with Western OEMs & how Western OEMs can respond

Chinese EV makers’ software organizations have long been secretive and functioned exclusively in China. However, their size and publicity have grown, especially among younger software talent, with the stagnation of the rest of the Chinese tech sector.

Today, most Chinese EV makers rank within the top 30 most popular places to work for young Chinese talent.

However, what’s next for Chinese EV makers is not a larger share of software talent in China but a larger share of software talent in the West.

There are 2 main reasons for this strategic shift:

Chinese EV makers are well prepared for this expansion, as they have closely followed Western OEMs entering China and their struggles to keep up with domestic brands due to software issues. This is a mistake Chinese EV makers don’t want to repeat when entering Western markets.

As of April 2024, no Chinese EV maker has significantly expanded into Western markets. Traditionally, the overwhelming majority of base-layer Chinese EV software has been built by Chinese engineers in China, while the more complex software components have been purchased from Western Tier1s.

However, in recent years, this has changed as the components that Chinese EV makers previously purchased by Western Tier1s are being developed in-house.

An example of this trend is Chinese BYD changing their ADAS environment from purchased from Bosch to one developed in-house. This announcement came in May 2023 when BYD announced it was setting up an intelligent driving research division in Shanghai. Not even one year later, in January 2024, they announced they’d launch it during the spring 2024.

The ADAS division, which was small and scattered before, has grown into a behemoth, with 4,000 employees (1,000 algorithm & hardware engineers and 3000 software engineers), revealed at the BYD Dream Day in January 2024.

At the BYD Dream Day, the company also revealed the headcount of its Research and Development organization for the first time, including its plan for a move from software-defined mobility to AI-defined mobility.

Here’s an overview of BYD’s total R&D headcount of 90,000 employees spread across 10 departments:

BYD is also heavily investing in AI, which is divided into Core AI, and Leading AI

Core AI: Self-research and development, empowering the next generation

Leading AI: Advanced algorithms, big data analysis, cloud computing, and edge comput

The goal of BYD’s AI-defined vehicle intelligence is to achieve smooth communication between various systems. BYD benefits from independently building the core technology of the entire new energy vehicle (NEV) industry chain, achieving full-stack self-research from hardware to software.

To achieve vehicle intelligence, BYD uses the brain as the core and links the neural network to launch the vehicle intelligence and electronics integration architecture (the “Xuanji Architecture”). The Xuanji architecture consists of one brain, two ends, three networks, and four chains:

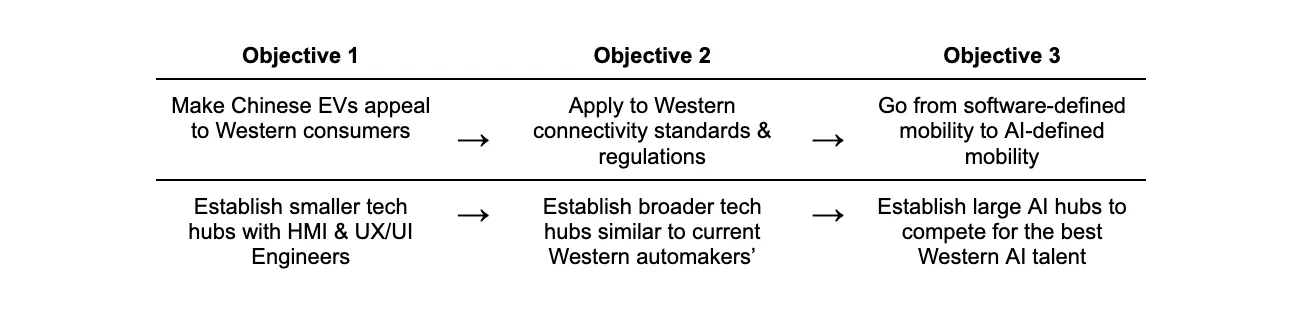

When it comes to selling cars in the Western markets, Chinese EV makers (BYD, Xpeng, NIO etc.) have realized that they need to rebuild their software organizations for international expansion.

From a strategy point of view, Chinese EV makers have 3 main objectives when moving into Western markets and will set up their tech hubs accordingly:

The first objective for China’s EV makers is to establish consumer trust and sales. This is done by adapting the Chinese consumer experience to Western markets by hiring HMI engineers and UI/UX designers.

Secondly, Chinese EV makers need to adapt to Western connectivity standards and regulations to fit into the ecosystem and the services. For this, they need roughly the same engineers as Western OEMs.

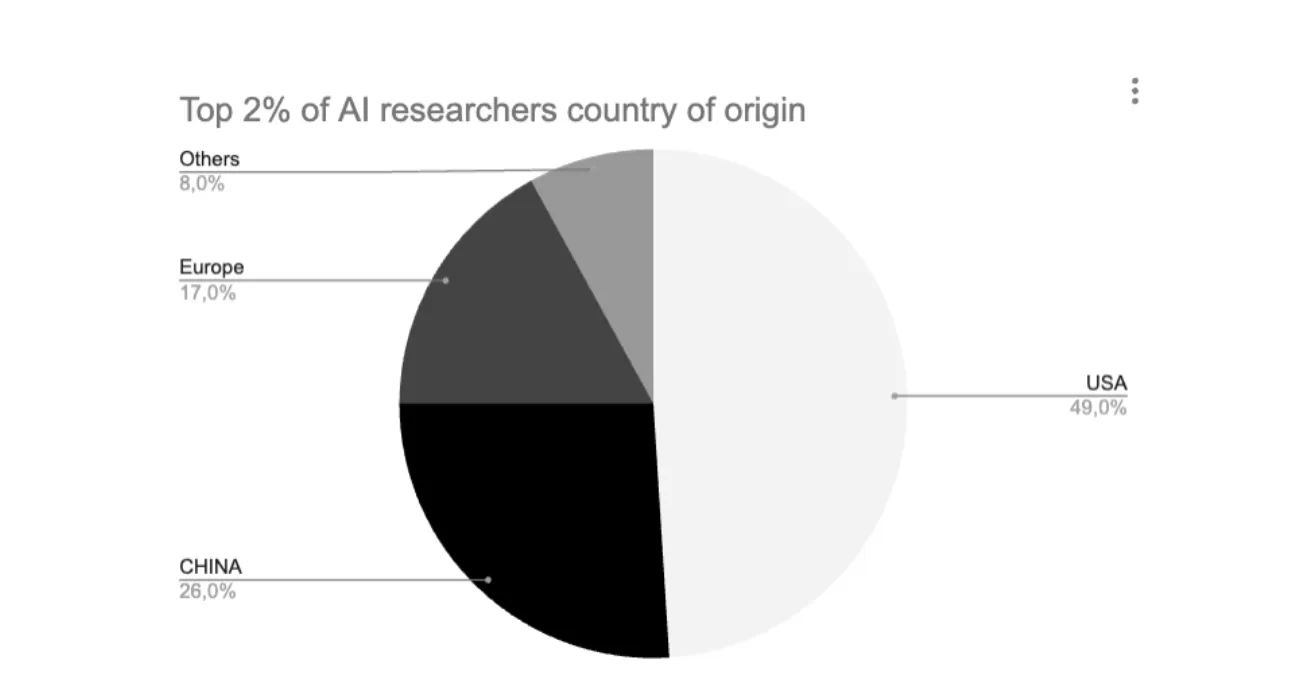

Thirdly, Chinese EV makers will establish large AI hubs to compete in the new era of AI-defined mobility by accessing roughly ¾ of the world's AI engineers who currently reside in Western markets.

When Chinese EV makers expand by building Western tech hubs, they immediately start to pull talent from Western automakers, often with superior compensation.

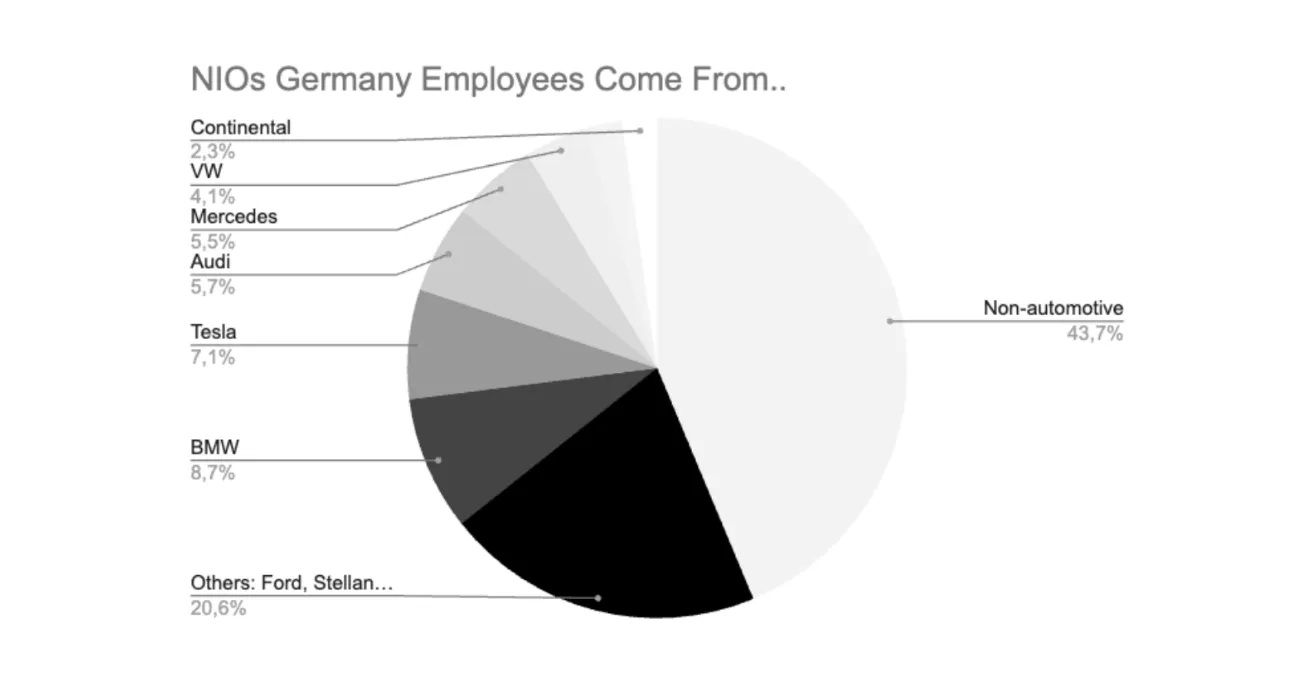

On April 8th, 2024, NIO opened a new tech hub in Schönefeld, near Berlin. Before that, NIO had already had a presence in Europe prior to this for a couple of years.

During this time, more than ½ of NIOs Germany employees came directly from Western automakers.

Another route for Chinese EV makers is to expand their Western tech hubs by directly hiring from outside the sector, which will be highly relevant when expanding their AI hubs since the Western automotive sector has yet to establish large AI organizations of their own to be competitive in AI-defined mobility.

There are three main strategies Chinese EV makers take when entering the Western markets:

Expanding through acquisition: We have seen primarily Geely (owning Volvo Cars, Polestar, and Lotus) go down this route. The biggest benefits remain building on top of a brand that Western software talent already trust. The hard part is aligning the strategic development of two different companies under one roof.

Expanding through Western talent: NIO is a good example of a company that has built a Western image and a Western software organization. In the short term, this requires a bigger investment since it means starting from zero, but in the long term, it creates trust among Western software talent.

Expanding through Chinese talent located in the West: BYD is an EV maker that has previously almost exclusively served the Chinese market when it comes to passenger cars. Until now, their approach has been to build their Western software organisations with Western-located Chinese talent. It allows them to expand faster thanks to the familiar culture but makes it harder to develop for Western consumers and attract the best Western software talent in the long run.

The competition for the best software & AI talent is, in any case not easy for Chinese EV makers in Western markets. This is because Western automakers still have a base of familiarity, culture, and trust among Western engineers, which can’t be paid for by Chinese EV makers, but has to be earned over a longer period of time.

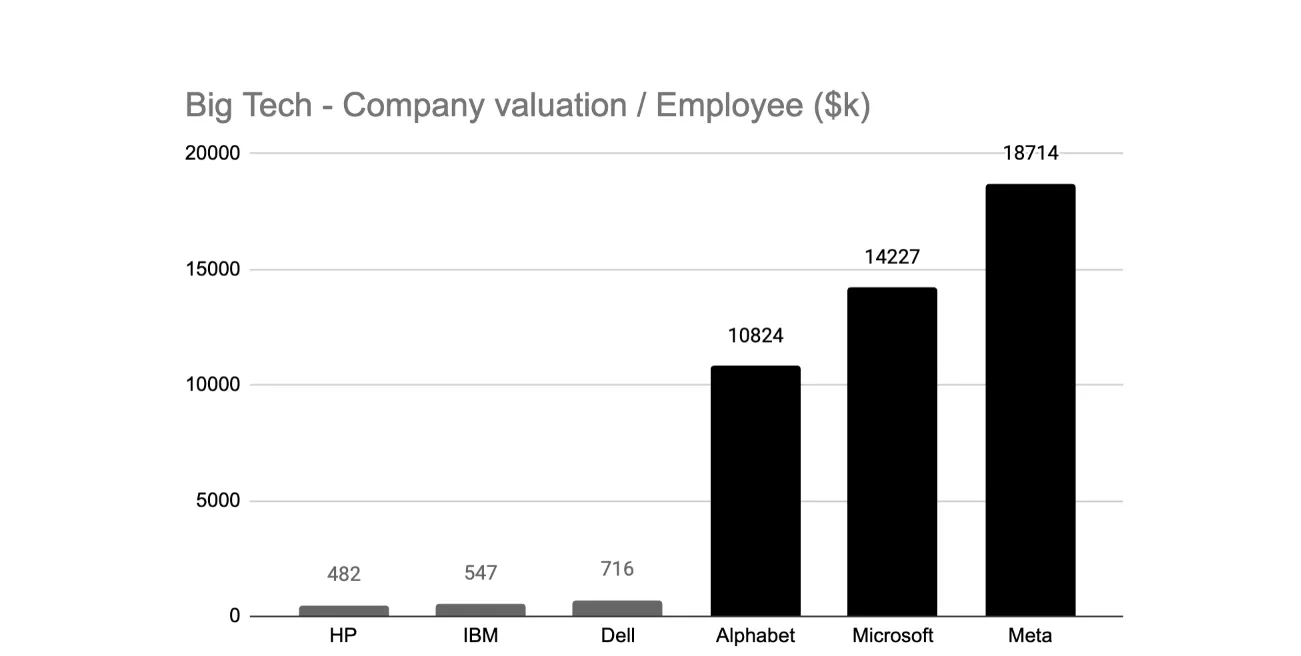

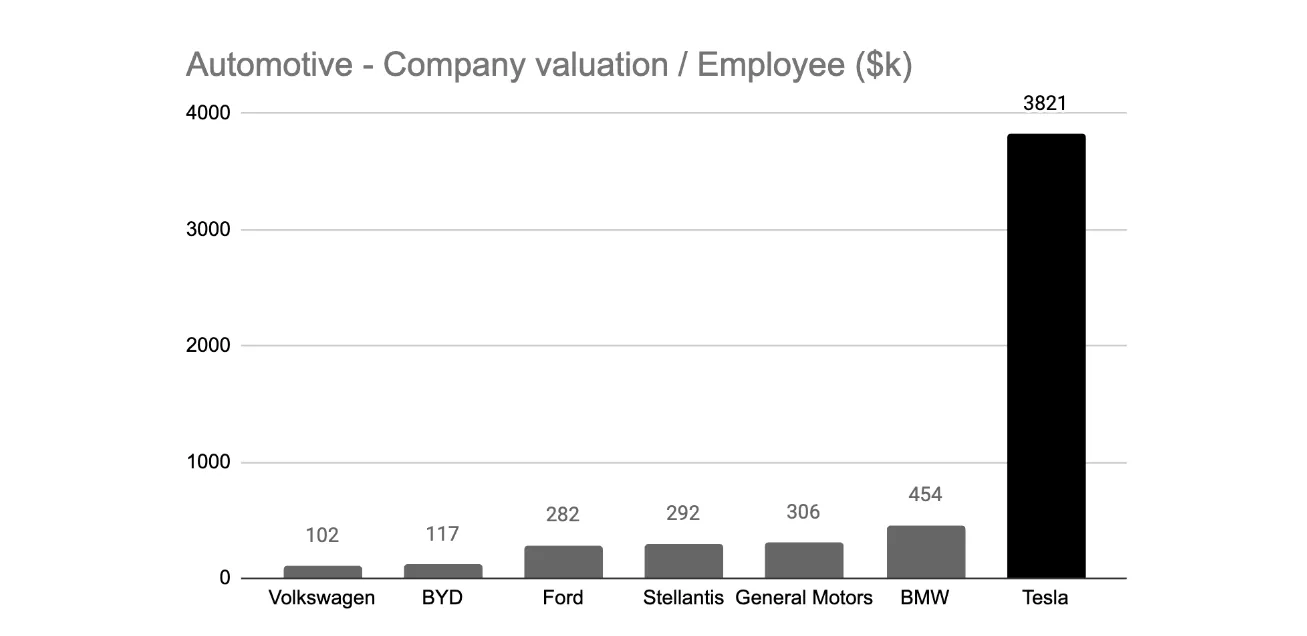

Companies with the world’s best tech talent often have an outsized valuation per employee compared to other companies in the same industry. We can clearly see this among Big Tech compared to traditional software companies.

The same can be seen in the automotive industry, with Tesla's valuation per employee being exponentially higher than other automotive companies.

A high concentration of “A-players” attracts other A-players, which creates a culture that attracts tech talent that can deliver exponentially more value, even when the individuals’ higher compensation is taken into account.

Conversely, organizations that increase headcount at all costs end up attracting B-players, who go on to hire C–players. This eventually results in a large, slow, and dysfunctional tech organizations

The best strategy for Western automakers to compete with Chinese EV makers when it comes to competing on software and AI talent is, interestingly enough, similar to what they should do when it comes to building cars: Focus on exponentially higher quality.

The automotive market will be taken over by a few companies that manage to build their software and AI organizations of A-players that can exponentially out-deliver organisations with bigger headcount but worse talent quality.

Finally, Western automakers quickly need a new methodology for building world-class software and AI organisations to compete.

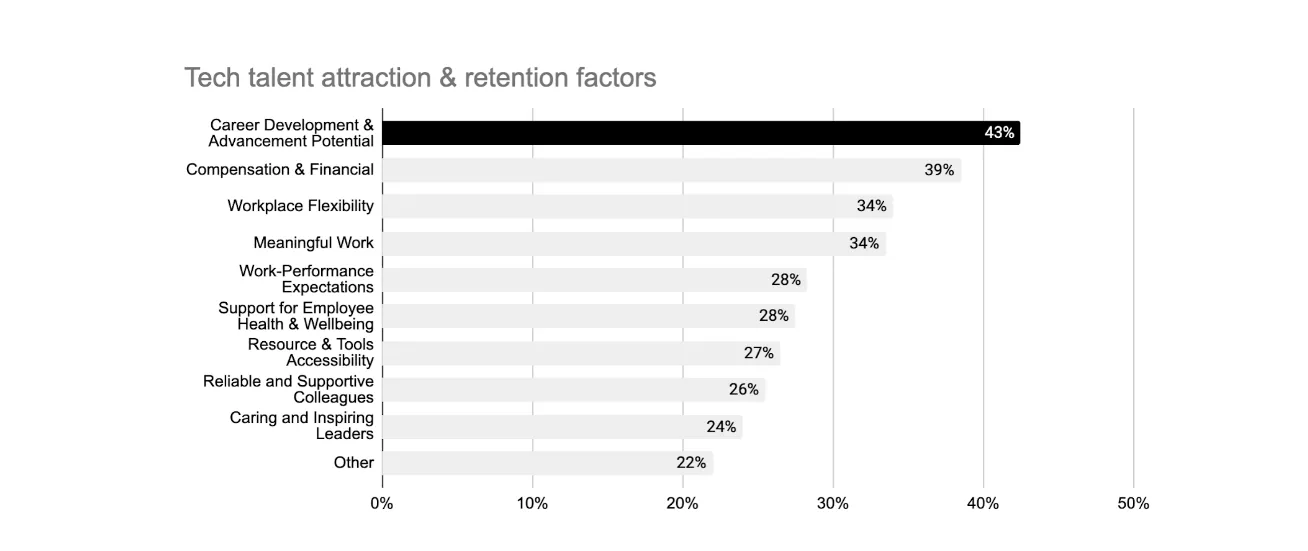

Compensation packages are not enough to attract top-tier tech talent. A recent study by McKinsey in 2023 revealed that Career Development and Advancement Potential was the number one factor for Attraction and Retention.

Top-tier tech talent is looking for career advancement and promotions, and the best way for them to do that is to switch firms regularly (tech workers change jobs every 2.7 years compared to 3.2 years for other professions).

Today’s tech talent wants to work on projects that interest them and move on to new ones when it’s no longer interesting. Switching between projects and companies allows them to build a broader knowledge base and get promoted faster compared to someone who stays in the same role & company for a long time.

The automotive industry has not previously been used to this quick circulation of talent and is plagued with heavy bureaucracy, long hiring times, and an unwillingness to offer competitive compensation for top-tier tech talent.

What can be done?

Automotive organizations need to adopt a hiring model that significantly decreases the time it takes to onboard new resources and not be afraid to let talent leave for other organizations when their project is done to make room for more suitable talent.

This new model is heavily based on flexible contracting, fast onboarding, and having a global on-demand pool of tech workers that can easily be tapped into for for projects when they come. Old employment models and costly re-skilling of the same employees for new projects need to be rethought to compete in a new age of automotive.

Hashlist is a global tech talent resourcing platform for the automotive sector.

Each month, Hashlist receives 5,000+ applications from the world’s best automotive-focused software and AI engineers.

Automotive companies use Hashlist to scale their software and AI talent organizations flexibly and cost-efficiently through a single partner globally.